Climate

The Graphic Truth: The rising (insurance) costs of climate change

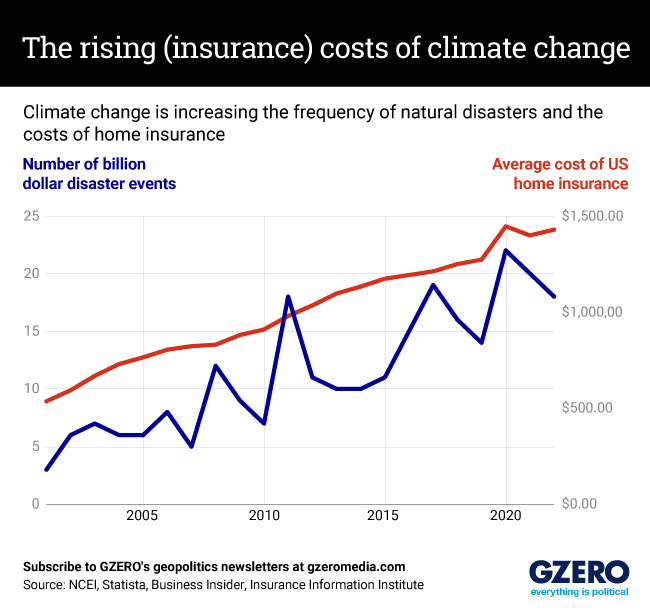

A line graph of the number of billion dollar natural disasters and US home insurance prices

Ico Oliveira

Between 1980 and 2021, the US endured an average of seven to eight natural disasters per year. In 2022, there were 18 disasters costing $175.2 billion in damages.

Increasingly frequent natural disasters are destabilizing the insurance market and turning it into a system where, in some places, only the most affluent can afford coverage. In 2021, FEMA, which had provided taxpayer-backed flood insurance nationwide, had to start setting rates equal to the flood risk. This change caused the average cost of flood insurance to jump from $888 a year to $1,808, with prices being exponentially higher for people living in flood zones.

Florida is on the verge of an insurance crisis after consecutive years of bad storms. Twelve private insurers in Florida have gone out of business since 2020, six in the last year alone, and 30 more are being monitored by state regulators because of their near-insolvent financial position.

Meanwhile, severe storms in the Midwest, drought and wildfires in the Southwest, and flooding in Kentucky and Missouri have priced hundreds of thousands out of the system in the last year alone.

In Louisiana, the insurance market has been buckling since Hurricane Katrina hit in 2005. After the last few years of bad storms, it has had to borrow $600 million to prop up insurers and rescue homeowners who have been abandoned by the broken system. The lack of insurance makes extreme weather events even more costly. It slows economic recovery, increases the likelihood of cascading financial consequences, and can leave people in financial ruin if their home is destroyed in an extreme event.

This is especially true in low-income communities, which are increasingly being left at the mercy of Mother Nature as natural disasters become more intense. Many of these vulnerable communities are being blue-lined, whereby banks or mortgage lenders designate neighborhoods that are more susceptible to climate risk and have less access to affordable insurance premiums. The practice has been found to cause home prices to plummet and is often happening to neighborhoods historically subjected to redlining – housing-related discrimination against communities of color – deeming them too risky to invest in.

Earlier in 2023, the Biden administration released a report detailing the economic challenges a warming planet posed to the US. They argued that bailing out homeowners after natural disasters incentivizes them to reside in riskier areas, increasing costs on taxpayers and slowing down climate change adaptations.

While the report is not legislation, it identifies how climate change has upended the nature of risk across the American economy and how the federal government will bear significantly higher costs in the future if it does not correct where it is creating “market distortions.” Two examples distortions the report identified were paying more for healthcare for victims of heat stroke and paying to rebuild coastal homes flooded by hurricanes.

The government wants climate change risk factored into Americans’ decisions, and insurance companies want it factored into their prices. But inevitably, those paying the biggest price will be low-income Americans with fewer resources to relocate.

Bill Maher says Donald Trump has pushed the limits of presidential power, but America's system of checks and balances is still holding.

In addition to the health concerns from the Ebola outbreak, the UN is sounding the alarm on a potential development crisis in Africa sparked by the disease.