On GZERO World, Ian Bremmer and former US Treasury Secretary Larry Summers discuss a range of topics, including the global banking system, the impact of AI on the labor market, and a controversial solution for rebuilding Ukraine.

On GZERO World, Ian Bremmer and former US Treasury Secretary Larry Summers discuss the policy response to the recent banking crisis involving Silicon Valley Bank and the Biden administration's actions.

Banks, in many ways, are the backbone of the economy, but when Silicon Valley Bank and Signature Bank recently failed, it raised some tough questions about the stability and regulation of financial institutions. On GZERO World, Ian Bremmer and former US Treasury Secretary Larry Summers dive deep into the crisis and explore the complex factors that led to the banking turmoil.

Much of what’s driving today’s banking drama—resulting in the most significant government intervention since the Great Recession—is a virus more contagious than COVID-19: panic, Ian Bremmer explains on GZERO World.

The recent spate of bank failures has caused significant turbulence in markets and left investors jittery across the globe, from Silicon Valley to Switzerland. But is this a sign of a systemic banking crisis or of a more fundamental flaw in capitalism? In an interview with Ian Bremmer on GZERO World, former US Treasury Secretary Larry Summers provides an in-depth analysis of the situation.

Listen: On the GZERO World podcast, Ian Bremmer and former US Treasury Secretary Larry Summers discuss the recent bank failures that are disrupting global markets and worrying investors worldwide. They discuss whether the current situation constitutes a banking crisis and explore the role of inflation in contributing to the problems. As an inflation expert, Summers provides valuable insights and predictions on the duration of the financial turmoil.

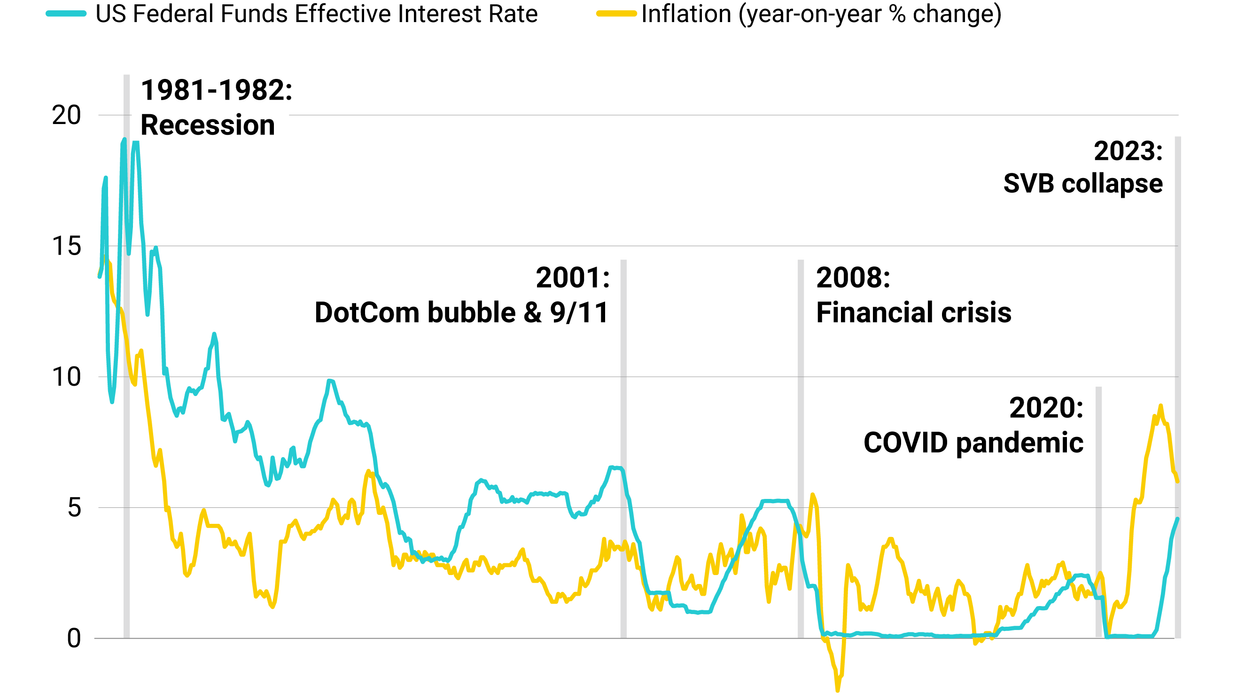

All eyes are on the US Federal Reserve, as it is set to announce Wednesday whether it’ll raise interest rates amid the recent banking turbulence.

The Fed’s decision will hinge on what central bankers think is a bigger priority: fighting inflation or stabilizing the financial sector following the recent collapses of Silicon Valley Bank and Signature Bank.

While it could stay the course in its inflation fight with another rate hike, the Fed is coming under growing pressure to ease investors’ anxieties by leaving interest rates be. But doing that risks giving in — temporarily, at least — to lasting inflation. The longer the Fed waits to control rising prices, the worse chance it has to reach its 2-3% inflation target without triggering a recession.

Also, high-interest rates are partly to blame for the recent financial turmoil on both sides of the Atlantic. Right-leaning critics argue that near-zero rates for too long made lending too cheap. Meanwhile, some on the left say that raising rates too quickly made borrowing too expensive, hurting the balance sheets of banks like SVB.

Who does Washington blame for the Silicon Valley Bank collapse? Jon Lieber, head of Eurasia Group's coverage of political and policy developments in Washington, DC shares his perspective on US politics.

With the Silicon Valley Bank collapse, is it 2008 all over again? As China reopens to tourism, is COVID finally behind us? Will the AUKUS deal shift the balance of power in the Indo-Pacific region? Ian Bremmer shares his insights on global politics this week on World In :60.