On the GZERO World Podcast, Ian Bremmer sits down with Harvard economist and former IMF Deputy Managing Director Gita Gopinath to unpack how the conflict is rippling through the global economy. As oil and gas prices surge, inflation is climbing, adding new costs for households and businesses and putting pressure on growth worldwide.

For sixteen years, Prime Minister Viktor Orban has won every fight: four consecutive parliamentary supermajorities for his party, Fidesz; a constitution rewritten to his specifications; courts, media, and oligarchs brought to heel.

In this episode of GZERO Europe, Carl Bildt examines how the war in Iran is driving up energy prices, fueling inflation, and raising stagflation fears across Europe.

Nearly a month ago, the US and Israel started a war with Iran. But one continent, which wants very little to do with the war, is uniquely impacted: Europe.

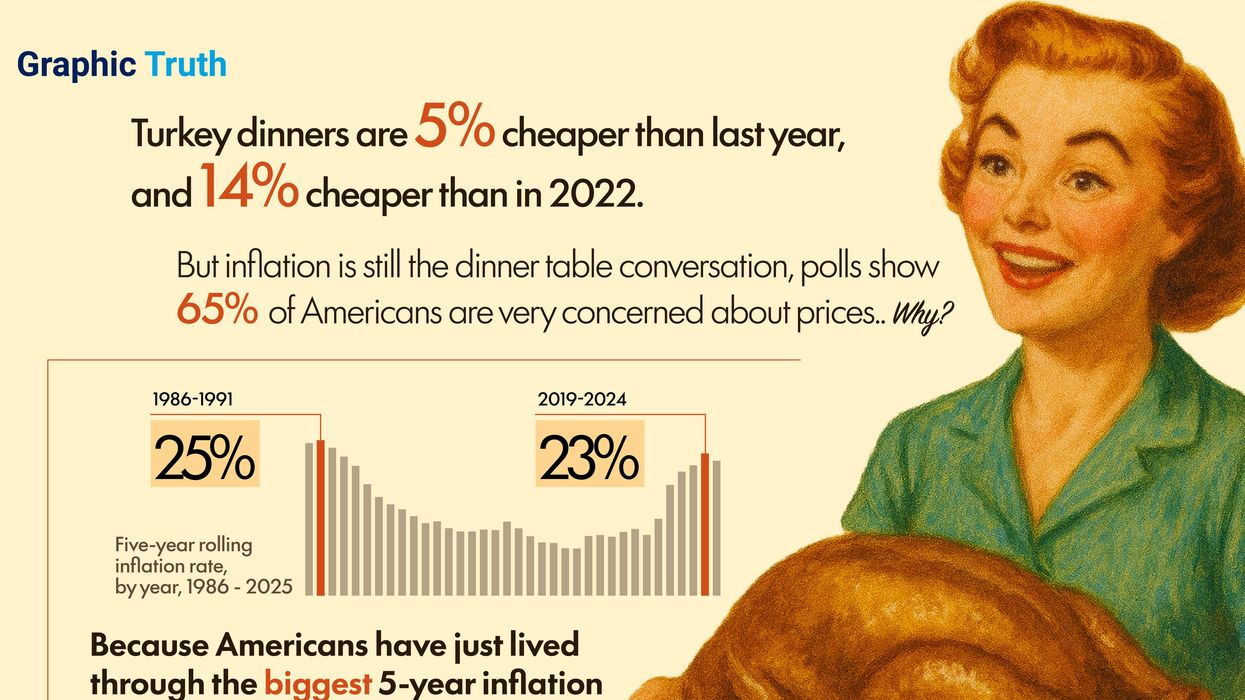

One thing to be grateful for this US Thanksgiving is that a turkey dinner for 10 people has gotten cheaper for the third year in a row. But nearly 65% of Americans are still upset about rising prices, according to a recent Pew Research Poll. How to reconcile those two things?